CITY DIARY

CHRISTOPHER FILDES

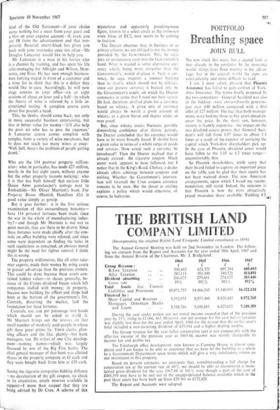

In a flurry of flying directors, whirling around the country in search of votes, the great struggle for Associated Electrical Industries is drawing to its close. Shareholders can and should remain on the ground. The pleasure with which they watch prices soaring ought to be tempered with scepticism. Have both com- panies really become worth so many millions of pounds more? 'Men may be wrong but the market never': which market? Act at 35s (this year's lowest point)—or AEI at almost double the price?

This astonishing turn of events is provoking two lines of argument. One says that perhaps most British companies have, like AEI, buried. treasure below. Was it (this argument goes) just the AEI management: or could many more boards of directors smartly improve the return on their capital if they were put to the proof? I think this is a dangerous proposition— especially when share prices have already risen by one third in just over a year—and it smacks of the lordly general condemnations of British business standards which come most freely from those who have never been exposed to the indignity of associating with mere commerce.

If you accept that, you should consider the second line of argument, which is that the fore- casts of higher profits—so profusely promised in a takeover situation—should meet some sort of check. I do not impugn either AEI's projec- tions or cEc's; but I remember a bid two years ago where the defending side made a profit forecast quite out of line with anything that had previously looked possible, and quite un- supported by detailed figures. The next year that company turned in a huge loss. Forecasts in such situations should meet the standards required in a prospectus; and where they do not shareholders should have a remedy against the forecasters at law.

If the sight of a wine list makes you feel (in Saki's words) like a schoolboy called upon to locate a minor prophet in the tangled hinter, land of the Old Testament—if your choice earns nothing but a sneer from your guest and

a blot on your expense account—if, even, you are JB from the advertisement and that tem- porarily flustered smart-Aleck has given you hock with your tournedos once too often—Mr Douglas Lancaster would like to help you.

Mr Lancaster is a man in his forties who is a chemist by training, and has spent his life sales-managing for Albright and Wilson, Mon- santo, and Esso. He has seen enough business- men looking stupid in front of a customer and a wine list to think that this is a defect they would like to cure. Accordingly, he will now stage courses in your office—six or eight sessions of about an hour and a half—in which the theory of wine is relieved by a little in- structional tasting. A complete course costs about five pounds a head.

This, he thinks, should come back, not only in more successful business entertaining, but also in better value for money—It'll also help the poor nit who has to pass the expenses.' A Lancaster course comes complete with samples, from a variety of wine merchants, but he does not teach too many wines at once: 'Well, hell, there's the problem of people getting drunk.'

Who are the 114 postwar property million- aires: who, in particular, has made £27 million, mostly in the last eight years, without anyone but the other property tycoons noticing: who it is that has built himself that curious little

Queen Anne gamekeeper's cottage next to Rothschilds—Mr Oliver Marriott's book The Property Boom (Hamish Hamilton 42s) is good value simply as gossip.

But it goes further: it is the first serious examination of this extraordinary bonanza—

have 114 personal fortunes been made since the war in the whole of manufacturing indus- try?—and though Mr Marriott is not out to point morals, they are there to be drawn. Since these fortunes were made chiefly after the con- trols on office building were relaxed, and since some were dependent on finding the holes in such regulations as remained, an obvious moral might be the need for tighter control. I think this is wrong.

The property millionaires, like all other take- over experts, made their money by using assets to greater advantage than the previous owners. This could be done because these assets con- tained hidden values—in shares generally, be- cause of the Cripps dividend freeze which left companies stuffed with money; in property, because new building for offices and shops had been at the bottom of the government's list. Controls, distorting the market, laid the foundation for these fortunes.

Controls, too, can put patronage into hands which should not be asked to wield it. Mr Marriott brings out the stresses on that small number of modestly paid people in whose gift these great prizes lie. Town clerks, plan- ning officers and the like, plainly—but bank managers, too. He writes of one City develop- ment—naming names—which was largely financed by one of the Big Five banks. The chief general manager of that bank was allotted shares in the property company at £1 each and they were bought back from him at £30 each.

Seeing the cigarette companies bidding defiance —no devaluation of the gift coupon, no check to its circulation, ample reserves available in support—I more than suspect that they are being advised by Dr Crux. A scheme of this mysterious and apparently pseudonymous figure, known to a select circle as the eminence vraie bleue of EC2, now seems to be coming to fruition.

The Doctor observes that, in business or as private citizens, we are obliged to use the money provided by the Government. This, he sass. puts an unnecessary card into the Governmen:'s hand. What is needed is some alternative cur- rency which, being more attractive than the Government's, would displace it. Such a cur- rency, he says, requires a sounder backing than its rival's; which should not be difficult, since our present currency is backed only by the Government's credit, on which the Doctor comments in terms that I need not here repeat. He had, therefore, drafted plans for a currency based on whisky. A given unit of currency would always be worth a given amount of whisky, at a given blend and degree under or over proof.

But, since whisky stocks fluctuate, possibly diminishing confidence after thirsty periods, the Doctor concluded that his currency would have to be more broadly based. It should have a given value in terms of a whole range of goods and services. How could such a currency be introduced? Then the Doctor realised that it already existed: the cigarette coupon. Much secret work appears to have followed, but I notice that in the King's Road. Chelsea, a dealer already offers arbitrage between coupons and steiling. Whether the Government's interven- tion will forestall the Crux coupon currency remains to be seen. But the threat to sterling explains a policy which would otherwise, of course, be ludicrous.