FINANCE AND INVESTMENT

By " CUSTOS "

THESE are not the days for ritualistic company meetings or for pee.rings into the trade horoscope. Everybody will therefore approve the banks' decision to reduce their meetings this year to more or less routine affairs and give us their chairmen's speeches in written form with the annual accounts. True to expectation, the war-time rise in deposits and its resultant influences on the banking position and the nation's finances is the central theme in most of the chairmen's reviews, Mr. McKenna, the Midland Bank chairman, describes the rise as part of "the general monetary expansion corresponding to the enlarged volume of production at a higher level of prices." Mr. Colin Campbell, chairman of the National Provincial, says much the same thing when he attributes the expansion of deposits to "the increased volume of Government borrowing and expendi- ture for war purposes."

DEFENCE OF BANK PROFITS

On the subject of banking profits Mr. McKenna makes a vigorous reply to the charge that the banks have been making unduly large profits out of what has been called " costless credit." All bank deposits, he reminds us, are paid for, partly in interest and partly in service, the cost of service, which has been sub- stantially increased by war difficulties, being ordinarily "much the greater." Of the £81,000,000 addition to the Midland Bank's deposits in 1940 as much as LH+ millions was used to fortify the cash position, bringing in no revenue; another La millions went into Treasury Bills, yielding i per cent.; - and L671 millions found its way into the new Treasury Deposit Receipts, on which the return is i per cent. On the whole £81,000,000 the bank earned less than I per cent., which was barely enough to cover the cost of the new deposits.

Mr. McKenna explained that the actual profits earned last year were "much the same" as in 1939, the fall in the published figure corresponding to the rise in taxation. Whether these earnings are a reasonable reward for services must not be judged by the 16 per cent, dividend on the paid-up capital. Thanks to past conservatism the banks have steadily increased the true capital funds employed. In the case of the Midland Mr. McKenna claims that the yield of something over 4 per cent. on the market value of the paid-up capital more accurately represents the return the shareholder receives on his actual capital than the 16 per cent, dividend rate. .

DEPOSITS AND WAR FINANCING

The survey of Mr. Rupert Beckett, Westminster Bank's chair- man, is concerned mainly with the rise in deposits as it affects war financing. Rather surprisingly he describes the large additions to the bank's resources since September, 1939, as "unwelcome." In his view the proper means of dealing with the increased savings created in war-time by abnormal disbursements of Government is the direct return of such funds to Government in the form of subscriptions to various loans. This process of direct lending to the State he considers to be "far preferable" to large increases in banking deposits, which merely shifts the problem of re-lending from the public to the banks. Since the problem does exist it is important that it should be tackled on lines which do not prejudice the liquidity of the banking position, and Mr. Beckett welcomes_the system inaugurated last year whereby banking resources are transferred to the Exchequer on 6 months' deposit receipts. This arrangement he regards as much more satisfactory than a wholesale addition to the bank's already large holdings of medium-dated Government stocks.

Analysis of the Westminster Bank's balance-sheet shows that, while deposits, at £410 millions, rose by 12 per cent., there was an increase of nearly £8 millions in the cash holding so that the cash ratio was up from 10.27 to 11.09‘ per cent. Total cash balances at December 31st were £64 millions and of the remaining £346 millions of the bank's resources as much as £220 millions was employed almost directly on Government account in Money at Call, Bills Discounted, Treasury Deposit Receipts and invest- ments in gilt-edged stocks. In addition, what 'Mr. Beckett described as a "large and increasing proportion" of the bank's advances was made to contractors engaged on Government account, to agriculture or in financing other activities vital to the war effort.

THE FALL IN ADVANCES

Mr. Colin Campbell, the chairman of the National -Provincial, is also at pains to explain that a large proportion of the bank's deposits is employed in financing the war. At December 31st just over a half of the deposit total involving a sum of £192 millions was in Treasury Bills, Treasury Deposit Receipts and stilt-edged (Continued on page 102p

FINANCE AND INVESTMENT

(Continued from page too)

stocks. In addition to this direct support of the nation's finances the bank was employing another Lto millions in money at all and short notice, practically the whole of which was lent in Lombard 'Street in helping the discount market to carry Treasury Bills. Analysing the fall in advances, which amounted last yen to nearly £20 millions, Mr. Campbell disclosed that in the case of the National Provincial nearly all classes of loans had contri- buted to this decline. One important factor was the control exercised by the Government in various commodity markets which has reduced the need for accommodation to merchants in importing and holding stocks. Another factor was the cessation of ordinary activities in certain trades such as those normally engaged in building and estate development. The banks and their customers had also co-operated in meeting the Treasury's wish that borrowings by private individuals for non-essential purposes should be stopped.

As a partial offset to these influences making for a lower level of bank advances, the total of loans to those engaged in the production of armaments and to other businesses engaged in the war effort have increased. Practically every new loan was for some purpose connected with the prosecution of the war, and the banks had also taken steps to ensure that no farmer who was in any way credit-worthy should be hindered in his opera- tions through want of financial facilities on reasonable terms. Mr. Campbell expressed the view that the trend towards a rathet lower level of bank advances would continue throughout the war,. but he had little doubt that there would be a big demand for loans after the war when it became necessary to finance the change-over of the vast industrial machine from war to peace conditions.

BARCLAYS BANK ACCOUNTS First among the "Big Five" to publish its full account; Barclays Bank shows a further substantial expansion of activities. Deposits have risen by more than k85,5oo,000, or about ift,per cent., and there have been corresponding increases in cash and

• other liquid items. Taking Cash, Money at Call, Bills Discounted and Treasury Deposit Receipts together, these amount to about 44 per cent. of deposits at December 31st. Like the other banks, Barclays shows a moderate decline in advances and a fall in its published profits after taxation. The dividend was com- fortably maintained, however, with £150,000 placed to con- tingency account and L200,000 to premises account.

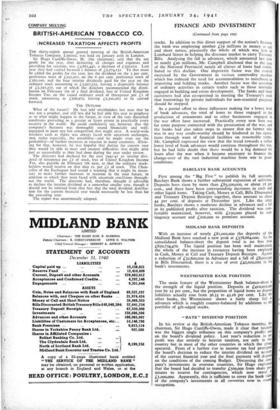

MIDLAND BANK DEPOSITS

With an increase of nearly L81,000,000 the deposits of the Midland Bank have reached a new peak at £578,664,000. In the consolidated balance-sheet the deposit total is no less than £650,734,470. The liquid position has been well maintained, the whole of the increase in resources having been employed in Cash, Money at Call and Treasury Deposit Receipts. Against a reduction of L32,60o,000 in Advances and a fall of L8,000,coo in Bills Discounted, there is a rise of over £42,000,000 in the bank's investments.

WESTMINSTER BANK POSITION

The main feature of the Westminster Bank balance-sheet 5 the strength of the liquid position. Deposits at Loo,000,od5? rose by 12 per cent., but the proportion of liquid items to deposit liabilities actually rose from 36.33 to 43.16 per cent. Like the other banks, the Westminster shows a fairly sharp fall In advances which is roughly counter-balanced by additions to the portfolio of gilt-edged stocks.

" BATS " DIVIDEND POSITION

In his review at the British-American Tobacco meeting, the chairman, Sir Hugo Cunliffe-Owen, made it clear that taxation was the biggest single influence on this company's profits and on the board's dividend policy. Last year's reduction in net profit was due entirely to heavier taxation, not only in this country but in most of the other countries in which the grout) operated. Fears of a further rise in income tax had prompted the board's decision to reduce the interim dividend on account of the current financial year and the final payment will dePend on the conditions of the coming Budget. Discussing the corn' pany's investments in overseas countries, Sir Hugo explaiited that the board had decided to transfer L5oo,000 from share Pre' miums to reserve for contingencies, which now stood at Li,000,000. Apparently, this is sufficient to cover the book value of the company's investments in all countries now- in ellen occupation.