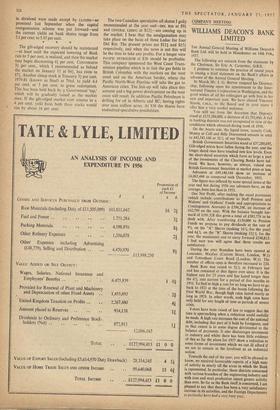

COMPANY NOTES

By CUSTOS

TUESDAY brought a slight check to the upward movement on the Stock Exchange but the market remains very firm, except in oil shares, which hang nervously on politics. When sentiment changes at a stroke almost from bearishness to bullishness, a large pent-up demand for invest- ments is suddenly released, as is shown by the increase in dealings from the 8,000 daily to nearly 16,000 on Monday. But a warning must be sounded. The buying is highly selective—gilt- edged, the attractive new issues (Tanganyika 5* per cent. was ten times over-subscribed and opened at 24. premium), and the electrical-power group which the new Government is boosting. When disappointing company reports are issued the market quickly comes back to realities.- For example, WOOLWORTH'S report revealed a flatten- ing-out of profits and although the dividend went up, as expected, to 60 per cent. the absence of a scrip bonus disappointed the bulls and the shares came back from 63s. to 60s. (to yield 5 per cent.). By contrast MARKS AND SPENCER have risen to 74s. cum the 100 per cent. scrip bonus (against 60s. before bonus). Another sign of selectivity is that the boom in the gilt-edged market has hardly affected bank shares. The joint stock banks did not do as well last year as the optimists expected, although an increase of 9.2 per cent. in net earnings (against 6 per cent. in 1955) is not to be despised. The highest rate of increase in profits was 10.3 per cent. for BARCLAYS and the lowest-7.9 per cent.—for the NATIONAL PROVINCIAL, which alone of the 'big five' main- tains the traditional practice of valuing its securities at or below market prices. No increases in dividend were made except by LLOYDS—U promised last September when the capital reorganisation scheme was put forward—and the current yields on bank shares, range from 5.1 per cent. to 5.45 per cent.

The gilt-edged recovery should be maintained —at least until the expected lowering of Bank rate to 5 per cent. is realised, and then• the market may begin discounting 41 per cent. CONVERSION 31 per cent., which I recommended as behind the market on January 11 at 841, has risen to 87+. Another cheap stock is Treasury 31 per cent. 1979-81 (known as Steel) at 79xd. to yield 4.4 per cent, or 5 per cent. to gross redemption. This has been held back by a Government 'tap,' which will be gradually raised as the market rises, If the gilt-edged market ever returns to a 4 per cent. yield basis both these stocks would rise by about 16 per cent. The two Canadian speculative oil shares I gaily recommended at the year end—DEL RIO at $91 and CENTRAL LEDUC at $121—are coming up in the market. I hear that the amalgamation may take place on the basis of three Leduc for four Del Rio. The present prices are $11+ and $151 respectively, and when the news is out this will be the time to take any profits. For a longer view PACIFIC PETROLEUM at $36 should be profitable. This company sponsored the West Coast Trans- mission pipeline which is to link the gas fields in British Columbia with the markets on the west coast and on the American border, where the Pacific North-West Pipeline will take the gas to American cities. The link-up will take place this autumn and a big power development on the west coast will result. In addition Pacific Petroleum is drilling for oil in Alberta and BC, having rights over nine million acres. At $36 the shares have undoubted speculative possibilities.