like emig tle t h i

SCARCELY any of the solid investments, indeed w

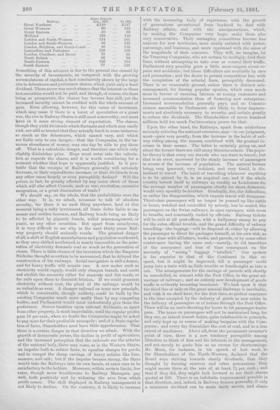

Stocks of the great English Railways. Almost everything, it measure his character by his sympathies, we must take them as is true, has risen, especially of late, till grave financial writers they were. We cannot found our estimate on one-half of his work, calculate that of the three thousand millions sterling, or there- His influence, we fully believe, was purer than his ideal. By abouts, dealt in on the Stock Exchange, the total saleable value that blessed pre.emiuence of good which is often hidden by the has increased within two years by six hundred millions ; but greater immediate forcibleness of evil, what was lofty and in- still, the special rise in Railways is very remarkable.

Great Northern Blum nice in Jun., 187.5.

£110

In 1831.

Great Western 60

132 Great Eastern 38

68 Midland 123

140 London and North-Western 124

161 London and South-Western ... 93

139 Loudon, Brighton, and South-Coast 46

142 Lancashire and Yorkshire .„ 128

136 London, Chatham, and Dover 15

32 North British 36 ... 90 North-Eastern 126 „. 174 South-Eastorn ".

77

... 138

Something of this advance is due to the general rise caused by the security of investments, as compared with the growing accumulations of capital, a fact conclusively shown by the large rise in debentures and preference shares, which yield only a fixed dividend. There never was much chance that the interest on these last securities would not be paid, and though, of course, the lines being so prosperous, the chance has become less still, yet the increased security cannot be credited with the whole amount of gain. Even allowing, however, for this cause of increment, which may cease if there is a burst of speculation or a great war, the rise in Railway Shares is still most noteworthy, and must have in it some strong element of expectation. The shares, though they yield divideuds which fluctuate and which may easily sink, are still so trusted that they actually fetch in some instances as much as the debentures, which cannot vary, and which are liable only to one danger,—that the Companies, in the im- mense abundance of money, may one day be able to pay them off. That is a calculable danger, and therefore one which only slightly diminishes price. Hope must enter into the calcula- tion as regards the shares, and it is worth considering for a moment whether that hope is apparently justified. Is it pro- bable that the receipts of Railways generally will seriously decrease, or their expenditures increase, or their dividends from any other cause largely or even perceptibly declineP Will the prices, in fact, be greatly affected by any cause short of those which will also affect Consols, such as war, revolution, excessive emigration, or a great diminution of trade P

We should say, on the whole, that the probabilities were the other way. It is, we admit, nonsense to talk of absolute security, for there is no such thing anywhere, laud at this moment being a risky investment, all State debts liable to im- mense and sudden increase, and Railway bonds being as likely to be affeeted by gigantic frauds, wilful mismanagement, or panic, as any other securities. But apart from cataclysms, it is very difficult to see why in the next thirty years Rail- way property should seriously recede. The greatest danger of all, a shift of English manufactures and population southward, as they once shifted northward, is nearly impossible, as the geue- ration of electricity demands coal as much as the generation of steam. There is little chance of the invention which the Emperor Nicholas thought so certain to be announced, that he delayed the construction of his railways. Aerial navigation is still a dream, and for heavy traffic will remain one. A new motor such as electricity would supply, would only cheapen transit, and could not abolish the necessity either for separate and fiat roads, or for rails upon them to diminish friction. If we could generate electricity without cost, the plant of the railways would be as valuable as ever. A cheaper railroad on some new principle, which is conceivable, though unlikely, could be built by the existing Companies much more easily than by any competing bodies, and Parliament would most undoubtedly give them the preference. Severe taxation upon railroad dividends, as apart from other property, is most improbable, until the regular profits pass 10 per cent., when no doubt the Companies might be asked to pay more for their profitable monopoly; and of a State regula- tion of fares, Shareholders need have little apprehension. That there is a certain danger in that direction we admit. With the growth of democratic power, the decline in profit of agriculture, and the increased perception that the railroads are the arteries of the national body, there may come, as in the Western States, an impulse both to reduce fares, to equalise charges for goods, and to compel the cheap carriage of heavy articles like lime, manure, and salt; but if the impulse became strong, the State would take the Railways into its own hands, at rates sure to be satisfactory to the holders. Moreover, within certain limits, low rates, though more troublesome to Railway Managers, pay well, both positively and by widening the area from which profit comes. The skill displayed in Railway management is not likely to decline. On the contrary, it is likely to increase with the increasing body of experience, with the growth of generations accustomed from boyhood to deal with Railway affairs, and with the amalgamations, which, by making the Companies very large, make them also very conservative. Their managing committees become less anxious for now territories, more nearly satiated with power, patronage, and business, and more oppressed with the sense of the magnitude of their concerns. They will, we imagine, let the Tramway Companies, who are certain to multiply, feed their lines, without attempting to take over or control their traffic. Parliament may possibly grow a little more exigent about re- pairs and accidents ; but those difficulties are avoidable by care and. precaution ; and the desire to permit competition has, with the completion of the arterial lines, perceptibly decreased. There is no reasonable ground, unless there is distinct mis- management, for fearing popular opinion, which runs much more in favour of ensuring fairness as among customers and increased accommodation than of fostering new enterprises. Increased accommodation generally pays, and no Commis- sioners amenable to Parliament are likely to force improve- ments not absolutely necessary to security, and certain greatly to reduce the dividends. The Shareholders of seven hundred millions hold too much Parliamentary power for that.

Upon the other hand, the Railways, apart from misfortune seriously reducing the-national resources, may—in our judgment, must—gain very greatly, from the increase in the habit of rail- way riding among the masses, combined with the gradual in- crease in their means. The latter is certainly going on, and about the former there are still many illusions extant. The popu- lar theory is that every one travels who can want to travel ; but that is an error, answered by the steady increase of passengers in excess of the increase of population. The natural human being, very ignorant, very indolent, and very timid, is dis- inclined to travel. The habit of travelling whenever anything is to be gained by it, is an acquired one, and if the whole country betook itself to railways as readily as Londoners do, the average number of passengers, chiefly for short distances, would very speedily be doubled. Gradually, too, the difficulties, or rather the disagreeables, which impede travel will disappear. Third-class passengers will no longer be penned up like cattle in boxes, watched and controlled by nobody, but be seated, like passengers on the Swiss railways, in open carriages, with room to breathe, and constantly visited by officials. Railway tickets will be sold at all post-offices, with a halfpenny stamp to pay for the extra official trouble, and the grand difficulty of railway travelling—the luggage—will be disposed of, either by allowing the passenger to direct his packages himself, at hie own risk, as is now done with all letters, books, and parcels, or by some other contrivance having the same end,—namely, to rid travellers of the annoyance and loss of time consequent on the

necessity of " seeing " luggage "labelled." Our system is far superior to that of the Continent in this re- spect, but it might be improved, till a passenger could j amp into a train with as little trouble or forethought as into a cab. The arrangements for the carriage of parcels will shortly be remodelled, in concert with the Post Office, to the great ad- vantage of railways ; and an entirely new development of goods traffic is evidently becoming imminent. We look upon it that the third line of rails on the great arterial Railways is inevitable, and with it we shall have, for the first time, as perfect exactness in the time occupied by the delivery of goods as now exists in the delivery of passengers or of letters through the Post Office. There will be no more shunting for hours to let passenger-trains pass. The taxes on passengers will not be maintained long, for they are, as inland transit duties, quite indefensible in principle, and only kept up as means of making bargains with the Corn- panics; and every day diminishes the cost of coal, and to a less extent of machinery. Above all, from the permanent investor's point of view, there is a new tendency perceptible among Directors to think of him and his interests in the management, and not merely to quote him as an excuse for shortcomings.

Mr. Moon, for instance, in his speech of last week to the Shareholders of the North-Western, declared that the Board were striving towards steady dividends, that they thought by forming reserves and other precautions they might secure them at the rate of, at least, 7A per cent.; and.

that if they did, they might look forward to see their shares quoted at 200. There is an indefinite improvement possible In that direction, and, indeed, in Railway finance generally, if only a minimum dividend can be made fairly secure, and share- holders, therefore, fairly patient. That once assured, it will be possible for Railway Companies, like States, to raise money at .3 per cent., even if they cannot venture to extinguish debt by terminable annuities. We look to it that if the Companies could but emancipate themselves from their necessity of dividing everything, could look to the value of their shares rather than the mere amount of their dividends, figures might be reached which to the Shareholders of 1870, almost ready to pray for State interference, would have seemed incredible. It is towards that position that the Railway Companies, as they become :solidified by time, tend to advance ; and before they reach it, it is quite possible that 2200 may be considered a low average price for shares.