The Dilemma of Interest Rates

By C. JOHN DUNHAM

SOME six million people have investment or mortgage accounts with building societies so it is hardly surprising that even the mention of a rise in interest rates can create a furore in the popular press. At such times the societies receive advice on what to do next from the popular press, and professional journals, from speakers and articles, and from building society borrowers themselves. Those offering it may be divided into two main groups, the advice given by one being precisely the opposite of that offered by the other.

One group consists of the ordinary borrower (and those sections of the press who support him). He has committed himself to a monthly payment which may well be as much as he can afford. He is understandably reluctant to pay more. The other group is made up of those economists, amateur and professional alike, who want a free society in which any move by the Government (say a rise in Bank rate) would immediately be reflected in rates of interest throughout the economy—including building societies. If, their argument goes, the Govern- ment wants to dampen economic activity, build- ing societies should co-operate by raising theil rates, and thus discourage new house construe tion and perhaps house purchase generally.

I would like here briefly to examine the factor: which determine building society mortgage and investment interest rates: and the first point want to make is that these rates are closely inter. related. Assuming the need to raise the invest• ment rate (the reasons for doing so are discussed below), an increase in the mortgage rate 13 bound to follow. This is because of the fine balance of building society finance.

Few people outside the movement realise just how fine this balance really is. Take the current situation. From the beginning of October most societies will be charging a rate of interest of 6 per cent. to their borrowers, new and existing alike. Of the £6 received in interest for each £100 lent, very little, perhaps only five or six shillings, is actual surplus and available for addition to reserves. This is shown by the following table which shows how the £6 will be spent by typical society after next October. Especially to be noted is the incidence of taxation and

the high proportion which it bears to the total.

s. d.

Paid to shareholders ..

3 10 0 Paid in taxation . •

1 12 0

Spent on management ..

12 0 Placed to reserve (surplus)

6 0

£6 0 0

What control can an individual building society, or the movement as a whole for that matter, exercise on these figures? Surprisingly little. The rate paid to shareholders is largely determined by external forces. The money re- quired to finance building society operations does not come from the big financial institutions of the country. It comes from ordinary men and women who have put their money into building society share or deposit accounts to provide for a rainy day or to save for something special, perhaps a house or a car or their child's future, or just so that their money is handy to meet household expenses. Now it is true that many of these investors tend to leave their money in their account with their favourite society year in and year out, but nowadays more and more are be- coming what we call 'interest rate conscious.' In other words, they go on the look-out for some- thing more profitable as soon as building society

rates become even slightly out of line with alternative forms of investment.

The current alternatives are shown in the fol- lowing table. It shows unmistakably that the recent decision to raise share rates to 31 per cent. was the right one. Shareholders as well as bor- rowers are members of building societies and their interests must always be taken into account.

COMPARATIVE YIELDS ON SMALL SAVINGS Equivalent Nominal grossed-up rate

I. BUILDING SOCIETIES

rate

s. d.

at 7s. 9d.

s. d.

(a) Shares .. • .

3 10 0 5 14 3 (b) Subscription shares 4 0 0 6 2 5 (c) Deposits .. .. 3 0 0

4 17

11

2 NATIONAL SAVINGS

(a) Savings Certificates

(Tenth Issue) ..

(b) Defence Bonds

(New Issue) ..

(c) Post Office and 4

5

3

0

11

0

6 5 17 12 1 6 Trustee Savings

Banks (Ordinary

Dept.):

First £600 .. 2 10 0 4 1 8

Remaining £4,400 (d) Special Investment 2 10 0 2 10 0 Department of

Trustee Savings

Bank 4 0 0 4 0 0

3. OTHER MEDIA (a) Commercial Bank Deposits ..

(b) Industrial Bank

3 0 0 3 0 0

Deposits (average) (c) Local Authority 6 0 0 6 0 0 Loans 5 10 0 5 10 0

[Note.—The table requires careful interpretation. Building Society subscription shares and National Savings certificates attract the full rate of interest only if held for given periods. No liability for sur- tax attaches to National Savings certificates, and interest on the first £600 invested in the Post Office Savings Bank or Trustee Savings Bank (Ordinary Department) does not attract income tax.] The next item, taxation, bears an arithmetical relationship to the other figures and cannot be altered independently. It includes some profits tax; so far, successive Governments have per- sisted in ignoring the societies' reasonable claim that it is unfair to tax their form of saving while granting relief to insurance company policy- holders and investors in Savings Certificates, the Post Office and trustee savings banks.

Some control can be exercised on management expenses but there is a limit to the saving which any economy measures may effect and, as the figures show, the proportion of income spent on management is small.

Reserves arc' the residual item : the total re- serve fund of a society is the accumulation of the small annual surplus over very many years of operation. If the ratio between reserves and total assets gets too small, the services the society can offer to the public must be curtailed for a period to allow the ratio to be improved.

So we are left with the mortgage rate. After October, 6 per cent. will be the basic rate as recommended by the Building Societies Associa- tion. Some societies will charge a slightly higher rate, usually because their small size compels them to pay a quarter per cent. more to their in- vestors. Others, quite reasonably, will charge an extra quarter per cent. if a borrower wants his loan over a longer term, say over twenty or twenty-five years. From the purely financial aspect, the position of building societies generallY could be greatly improved by further increasing the mortgage rate. Even an extra half per cent. would give more elbow room for manoeuvre by substantially bolstering reserves. The borrowing public and the popular press would obviously be opposed to such a move but let us, nevertheless, examine the case for it—a case, by the way, which is put by voices within the Movement as well as by some economists outside.

It is an established fact that the market would have borne a far higher rate of interest oa mortgages than has prevailed for some years now. One only has to look at those societies on the fringe of the movement who have charged and even 8 per cent. They have had no difficulty in finding borrowers and many of the houses on which the loans have been granted have been good substantial security. This immediately raises the question of whether it is worthwhile for potential borrower to take out a mortgage at 4 high interest rate. For most people the only alternative is to rent their home (if they can find a place) since comparatively few can purchase house outright. The fact is that it is worthwhile to buy your own house with the help of a building society and it would still be worthwhile if interest rates were far higher than they are now or likely to be. Over the last twenty years continuing inflation has led to an ever-upwards trend 'n property values, a trend which has far out- weighed any increases in mortgage interest. Ia overseas countries, borrowers are charged much higher rates than we are here. In Canada, for example, it is common to pay 7 per cent. or more for half of the amount borrowed and an exorbitant rate, perhaps 20 per cent. or more, for the rest. Despite all this, people there are willing and anxious to borrow, in order to have a house of their own.

Before the war, building societies were able to allocate proportionately twice as much to reserves as they can at present. A high margin now would act as a welcome shield against external in' fluences, so that changes in interest rates generallY would have less of an impact. The societies would not then be forced so often to take the unpopular and administratively expensive step of changing interest rates. This would not necessarily react unfairly on the borrower because rebates could be given to him in times when external interest rates were low.

Yet it is unlikely that mortgage rates will be raised much, if anything, above their present levels. Why is this? In the first place, housing is a necessity : it cannot be grouped with cars, re- frigerators, television sets and the like. It is an essential of life, like food and clothing, and as such takes priority over even roads, schools, hospitals and railways. And its cost must be kept down to a reasonable level. The special position which housing occupies in the economy has been recognised by the Government. Despite all the anomalies of rent restriction, it has been forced to impose a limit on its own policy of de' restriction, at least during the life of the present Parliament. Housing is too basic to be left un- protected in face of the economic storm. ManY would argue that the nation's present housing need is 200,000 new dwellings per year. A more realistic figure is double that number if any real inroads are to be made into the task of slum clearance. Clearly the housing programme cannot be set aside lightly; it should continue even though other parts of the economy have to be dampened down. In this light even 6 per cent. can be regarded as high.

In the second place, building societies do not exist to make profits: they exist to help people to buy their own homes. The mortgage rate must therefore be kept as low as possible. This is a matter of building society history and tradition; it is an important factor which has more than once proved decisive.

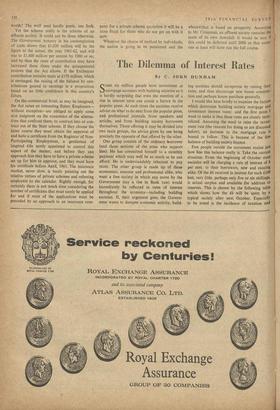

The objective of building society finance is therefore to strike a fair balance between the interest of both borrowers and investors and to equate, as far as possible, the inflow of funds with the demand for mortgage accommodation. In a relatively stable economy this problem is simple, once the right rates have been fixed. But w hat happens when interest rates generally change frequently? Historically, it can be shown that long-term rather than short-term changes in the level of interest rates have determined build- ing society rates. In particular, short-term fluctuations of Bank rate are not likely to count for much. Since 1952, Bank rate has mainly been used as it was before 1932, as an instrument of government policy to fight inflation, to protect reserves of gold and dollars and to regular economic activity. Building society borrowing and lending may for all intents and purposes be quite unaffected. As the following chart shows, history has proved that building society rates have tended to 'smooth out' the fluctuations in Bank rate. This is all to the good; Bank rate as well as credit squeezes and many other govern- ment measures can be clumsy weapons affecting deserving and undeserving causes alike.

Conversely, long-term changes in interest rates cannot be ignored indefinitely. Building society rates have tended to follow the same trend as the return obtainable on National Savings certificates and as the average annual yield on 21 per cent. Consols. Although building societies are non-profit-making and although they exist to promote home-ownership, they live in a free- enterprise world and cannot swim for long against the tide.

So there we have it. An investment interest rate which, if it is to be competitive, must be largely determined by forces external to the building society movement : and a mortgage rate whose lower level is fixed by the investment rate. Both rates must move in accordance with Ion! term trends in the level of interest generally. Th real dilemma comes when we try to find the rigl upper level for the mortgage rate. The 'marke t' would bear more than the 6 per cent, now charge d and the extra money would make a welcorr addition to reserves. But purely economic argt ments are not the only ones which weigh. Bulk ing societies have a marked sense of responsibilil 1-

y.

to their borrowers and a tradition of co-operatic which cannot easily be gainsaid.