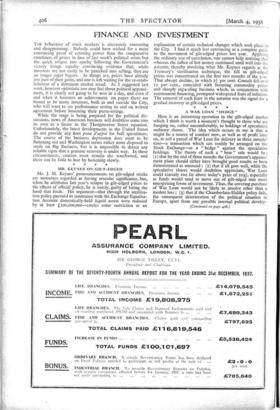

FINANCE AND INVESTMENT

Tint behaviour of stock markets is alternately reassuring and disappointing. Nobody could have wished for a more convincing proof of resisting power than the comparative steadiness of prices in face of last week's political crisis, but the quick relapse into apathy following the Government's victory brings equally convincing evidence that, while investors are not easily to be panicked into selling, they are no longer eager buyers. As things are, prices have already lost part of their gains, and one is left waiting for the re-estab- lishment of a dominant market trend. As I suggested last week, however optimistic one may feel about political appease- ment, it is clearly not going to be won in a day, and even if and when it becomes an achievement on paper there are bound to be many investors, both in and outside the City, who will want to see performance setting its seal on written agreement before loosening their purse-strings.

While the stage is being prepared for the political dis- cussions, news of American business will doubtless come into its own as a factor in the Throgmorton Street equation. Unfortunately, the latest developments in the United States do not provide any firm point d'appui for bull speculators. The course of the business depression does seem to be flattening out and Washington seems rather more disposed to smile on Big Business, but it is impossible to detect any reliable signs that a genuine recovery is under way. In these circumstances, caution must remain the watchword, and there can be little to lose by hastening slowly. * * * * MR. KEYNES ON GILT-EDGED Mr. J. M. Keynes' pronouncements on gilt-edged stocks are nowadays regarded as having oracular significance, but, when he attributes last year's relapse in gilt-edged prices to the effects of official policy, he is surely, guilty of biting the hand that feeds. His argument—that through the sterilisa- tion policy pursued in connexion with the Exchange Equalisa- tion Account domestically-held liquid assets were reduced by at least Lroo,000,000—carries some conviction as an explanation of certain technical changes which took place in the City. I find it much less convincing as a complete guide to the movement of gilt-edged prices last year. Applying the ordinary test of correlation, one cannot help noticing that whereas the influx of hot money continued until well into the autumn, thereby involving what Mr. Keynes regards as the Treasury's sterilisation technique, the fall in gilt-edged prices was concentrated on the first two months of the year. That abrupt decline, in which 21 per cent. Consols fell over per cent., coincided with booming comniodity prices and sharply expanding business which, in conjunction with rearmament financing, prompted widespread fears of inflation. The removal of such fears in the autumn was the signal for a gradual recovery in gilt-edged prices. * * * *

A WAR LOAN "HEDGE"

Here is an interesting operation in the gilt-edged market which I think is worth a moment's thought to those who are hanging on, rather uncomfortably, to holdings of speculative ordinary shares. The idea which occurs to me is that it might be a source of comfort now, as well as of profit later on, to sell a parcel of War Loan for delivery in three months' time—a transaction which can readily be arranged on the Stock Exchange—as a " hedge " against the speculative holdings. The theory of such a " bear " sale would be : (r) that by the end of three months the Government's appease- ment plans should either have brought good results or been demonstrated as unsound ; (a) that if all goes well, while the speculative shares would doubtless appreciate, War Loan could scarcely rise far above today's price of ro3, especially as funds would tend to move out of gilt-edged into more enterprising forms of investment. Thus, the covering purchase of War Loan would not be likely to involve other than a modest loss ; (3) that if the Chamberlain-Halifax policy fails, the consequent deterioration of the political situation in Europe, apart from any possible internal political develop-

(Continued on page 408.)

FINANCE AND INVESTMENT

(Continued from page 406.) ments, could scarcely fail to bring a sharp reaction in gia- edged as well as speculative share prices. In this unhappy event, the loss on the speculative holdings would be offset, wholly or partially, by the profit derived from repurchasing at a substantially lower price the War Loan sold threz months previously, thereby completing the bargain. * * * *

SOUTHERN RAILWAY PROSPECTS

Making due allowance for the one big " if " with which one must qualify most financial predictions nowadays—if a European upheaval is avoided—Mr. R. Holland Martin's address to Southern Railway stockholders was decidedly encouraging. Naturally, he reminded stockholders that receipts from steamboats, which had exceeded all expecta- tions in 1937, were closely dependent on the international situation and that consequently any adverse developments would be quickly reflected in a fall in net receipts. On the other hand, he pointed out that the general indications at present pointed towards a further expansion and that, in view of the rise in costs, the company had made an extra provision of io per cent. in the allocations to all its principal reserve funds. As a result of this policy, plus a transfer of f500,000 from the Fire Insurance Fund to the Improvements and Contingency Fund, reserves have been put in a healthy state to meet the extra cost of materials. Hence the board is hopeful of maintaining the deferred dividend at a steady level, with occasional upward movements. * * * * Frankly, this sounds just a little bit optimistic, although it will doubtless be well within the company's capacity provided conditions do not deteriorate. The yield of over 7 per cent. on the deferred stock, now quoted at 2ol, may reflect the market's mood of disillusionment rather than any serious attempt at intelligent anticipation, but I would still prefer the £6 6s. per cent. offered on the preferred at 791. This stock is surely undervalued, with a margin of £700,000 of net revenue behind its 5 per cent. dividend. * * * *

L .N.E .R . PREFERENCE POSITION

As I suspected, the full accounts of the London and North Eastern Railway, satisfactory as they are as 1937 history, introduce a slight element of doubt into this year's prospects. The implication of the preliminary figures is borne out that this company succeeded in 1937 in retaining net an abnormally large proportion of its gross improvement in the railway section. The net increase of £820,000 was equivalent to 37 per cent. of the gross increase. Add to this higher net receipts from the ancillary and miscellaneous sections and you have the basis of the impressive total net revenue rise of k966,000, which has enabled Second Preference holders to receive 1 per cent. By comparison with the London, Midland and Scottish and, in lesser degree, with the Great Western and the Southern, these results are very striking, but they need a little careful scrutiny. As I sug- gested last week, part of the apparent discrepancy must be attributed to differences in accounting methods.

The explanation of the relatively small rise in the L.N.E.R.'s total railway expenditure is to be found in the renewals charges. While maintenance of ways and works cost £273,819 more last year than in 1936, the maintenance charge for rolling stock was reduced, thanks to a net credit of £2,313,183, against £782,525, from rolling stock renewals funds. Thus a substantial rise in renewals costs has been offset by transfers from reserves. I do not think Second Preference holders need be alarmed at this position, provided other things remain equal, but equally I feel sure that they ought to keep this renewals problem in mind whenever they indulge hopes of a further improvement in revenue and dividend. The First Preference stock, to yield £6 8s. 6d. per cent., looks better value at 621 than the Second Preference at 23i.

Cusros.

[Readers' enquiries, or requests for advice, regarding particular shares will be answered periodically in print or by letter. Corre- spondents who do not desire their names to appear should append initials or a pseudonym to their questions.] (Financial Notes on page 410.)