FINANCE AND INVESTMENT

By NICHOLAS DAVENPORT

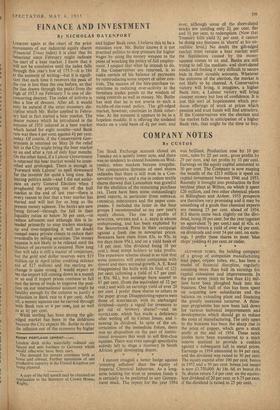

LOOKING again at the chart of the price movements of our industrial equity shares (Financial Times index) it is clear that its behaviour since February might indicate the start of a bear market. I know that it will not be conclusive until the index falls through this year's low of 175.7—it is ,184 at the moment of writing—but it is signifi- cant that each time it recovers the peak of the rise is less than the one before, so that the line drawn through the peaks from the high of 197.5 on February 3 is one of dis- concerting descent. The index of activity is also a line of descent. After all, it would only be natural if the strict monetary dis- cipline which Mr. Butler applied in Febru- ary had in fact started a bear market. The dearer money which he introduced in the autumn of 1951 ushered in a bear market which lasted for eight months—and Bank rate was then 4 per cent. against 4.3 per cent. today. Of course, if the Conservative Gov- ernment is returned on May 26 the relief felt in the City might bring the bear market to an end after a run of only four months. On the other hand, if a Labour Government is returned the bear market would be inten- sified and prolonged. There is enough in `Forward with Labour' to spell downward for the investor for quite a long time. But leaving politics aside—and I did not antici- pate an early General Election when I prophesied the petering out of the bull market at the end of last year—there is every reason to fear that a bear market has started and will last for as long as the Present money squeeze. The banks are now being forced—through the fall in their liquidity ratios to below 30 per cent.—to reduce advances and although this is in- tended primarily to stop traders stocking- up and over-importing it will no doubt compel many private clients to reduce their overdrafts by selling securities. The money squeeze is not likely to be relaxed until the balance of payments is restored. How long that will take is still a matter of conjecture. but the gold and dollar reserves were $19 million up in April (after crediting defence aid of $17 million) and the sterling ex-

and higher Bank rates. I believe this to be a mistaken view. Mr. Butler knows it is not practical politics to stop pressure for higher wages by using the money weapon to the point of wrecking the policy of full employ- ment. I suspect that what hp intends to do, if the Conservatives are returned, is to make certain of his balance of payments by reintroducing some import or other con- trols. The success of the hire-purchase re- strictions in reducing over-activity in the furniture trades points to the wisdom of using controls as well as money. Mr. Butler has said that he is not averse to such a middle-of-the-road policy. The gilt-edged market, however, continues to think other- wise. At the moment it appears to be in a hopeless muddle. It is offering the undated stocks on a yield basis of 43 per cent. and over, although some of the short-dated stocks are yielding only 23 per cent. flat and 33 per cent. to redemption. (Now that Treasury bills yield 33 per cent. it cannot be doing any business in 'shorts' at his un- realistic level.) No doubt the gilt-edged market must remain a bear market until the liquidation caused by the money squeeze comes to an end. Banks are still trying to sell the medium- and short-dated stocks and finding it very difficult to secure bids in their sizeable amounts. Whatever the outcome of the election, the market is not likely to be cheered. A Conservative victory will bring, it imagines, a higher Bank rate; a Labour victory will bring cheaper money but loss of confidence. It is just this sort of hopelessness which pro- duces offerings of stock at prices which pension and trust funds will find attractive. If the Conservatives win the election and the market falls in anticipation of a higher Bank rate, that might be the time to buy.